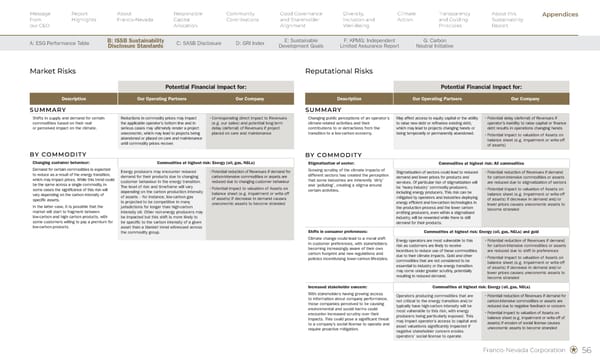

Climate-Related Risks and Opportunities As a royalty and streaming company, Franco-Nevada does not operate mining or energy assets and is therefore not directly exposed to many of the climate-related operational risks faced by operators. However, climate-related physical and transition risks and opportunities affecting our operating partners can indirectly impact Franco-Nevada, including through changes in production levels, development timelines, asset viability and commodity market dynamics. These impacts may, in turn, influence royalty and stream deliveries, revenue timing, asset valuations and long-term portfolio performance. Consistent with our long-duration, buy-and-hold investment model, Franco-Nevada evaluates climate-related risks and opportunities ("CRROs") over short-, medium- and long-term horizons, recognizing that different risk drivers may materialize at different points over the life of our assets. Acute physical risks typically arise over shorter timeframes, while chronic physical risks and many transition-related risks, such as policy, legal, market and reputational factors, may evolve over longer periods and influence strategic outcomes and capital allocation decisions. Climate Scenario Analysis Climate-related scenario analysis is a key tool used by Franco-Nevada to assess the resilience of our business model and strategy to CRROs over the short, medium and long term. In line with the IFRS Sustainability Disclosure Standards, and in particular IFRS S2, scenario analysis is used to inform our understanding of material climate- related uncertainties, how these may evolve under different climate pathways, and how they could affect our operating partners, assets and long-term prospects. In this section, we have updated and expanded our climate-related scenario analysis, with a primary focus on alignment with IFRS S2. This work underpins our updated identification and assessment of climate-related physical and transition risks and opportunities, as well as an enhanced assessment of the resilience of our strategy and portfolio. The analysis reflects Franco-Nevada’s royalty and streaming business model, including our non-operating role and long-term asset exposure, while drawing on reasonable and supportable information available as at the reporting date. The scenario analysis incorporates multiple climate pathways and time horizons consistent with IFRS S2 guidance. These scenarios draw on widely used international reference datasets and frameworks, including those developed by the IPCC, NGFS and IEA, and consider both transition and physical CRROs across Franco-Nevada’s key commodities and regions. A detailed description of the scenarios selected, key assumptions, time horizons, methodologies, findings, and limitations is provided on the following pages. Integrated Approach In this reporting period, and in line with the IFRS Sustainability Disclosure Standards, Franco - Nevada has integrated its assessment of CRROs with climate scenario analysis to better understand how these risks and opportunities may develop under different climate pathways and how resilient our portfolio and strategy may be over time. A total of 11 CRROs, spanning physical and transition factors, were assessed through scenario analysis. Of these, seven were identified as having potentially significant financial implications for Franco - Nevada and are therefore included in this disclosure. CRROs assessed but not disclosed reflect lower perceived financial materiality at this time and include, for example, acute and chronic heat - related impacts causing production disruption and reduced productivity, and changes in customer behaviour related to oil, natural gas, iron ore and gold. This integrated approach reflects the expectations of IFRS S2, which emphasizes the use of scenario analysis to inform the assessment of material climate - related uncertainties, strategic resilience and future prospects, rather than treating scenario analysis as a standalone exercise. The updated scenario analysis that follows underpins our identification and prioritization of significant CRROs across key commodities and regions and informs our understanding of how these factors could affect our operating partners and Franco-Nevada under different future conditions. This approach supports our capital allocation discipline and ongoing evaluation of portfolio resilience, while remaining proportionate to Franco-Nevada’s non-operating business model and reliance on third-party operators. Climate-Related Risks, Opportunities and Portfolio Resilience | Implications for Franco-Nevada’s business model, strategy and financial resilience Our Approach to Scenario Analysis 1. Prioritization of Key Commodities and Regions 2. Identification and Prioritization of Risks and Opportunities 3. Assign Indicators and Data Collection 4. Climate Trend Analysis 5. Analysis and Implications for Franco-Nevada’s Value Chain Six key commodities and 14 geographic regions were prioritized based on financial materiality, asset concentration, production volumes, and sensitivity to climate - related physical and transition drivers, focusing on areas most likely to experience material CRRO impacts across Franco - Nevada’s value chain. A review of internal documentation, a targeted information request, and a stakeholder workshop refined a long list of CRROs into 11 priority items—four physical risks and seven transition risks and opportunities—for inclusion in the scenario analysis. Selected scenarios and time horizons were applied, with each priority CRRO mapped to relevant climate indicators. Associated climate data were sourced from leading global datasets, including the IPCC, ISIMIP, WRI, NGFS, and the IEA. Scenario - based climate data were analyzed to assess projected changes over time for each CRRO across prioritized commodities and regions, evaluating the magnitude and direction of indicator changes to determine potential financial significance. Based on the analysis, impact and likelihood ratings were assigned to each CRRO in line with Franco - Nevada’s enterprise risk framework, supported by qualitative commentary describing how risks and opportunities may evolve and affect Franco - Nevada and its operating partners over time. Franco-Nevada Corporation 56

Sustainability Report 2025 Page 57 Page 59

Sustainability Report 2025 Page 57 Page 59