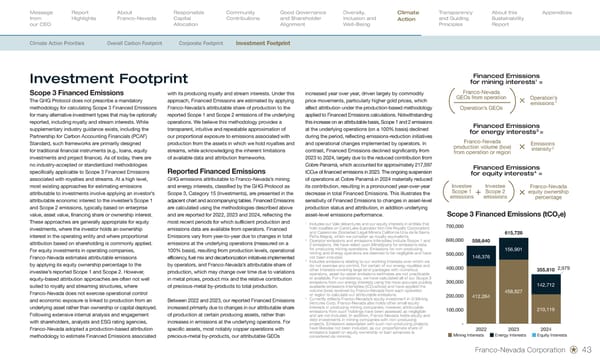

Investment Footprint Scope 3 Financed Emissions The GHG Protocol does not prescribe a mandatory methodology for calculating Scope 3 Financed Emissions for many alternative investment types that may be optionally reported, including royalty and stream interests. While supplementary industry guidance exists, including the Partnership for Carbon Accounting Financials (PCAF) Standard, such frameworks are primarily designed for traditional financial instruments (e.g., loans, equity investments and project finance). As of today, there are no industry - accepted or standardized methodologies specifically applicable to Scope 3 Financed Emissions associated with royalties and streams. At a high level, most existing approaches for estimating emissions attributable to investments involve applying an investor’s attributable economic interest to the investee’s Scope 1 and Scope 2 emissions, typically based on enterprise value, asset value, financing share or ownership interest. These approaches are generally appropriate for equity investments, where the investor holds an ownership interest in the operating entity and where proportional attribution based on shareholding is commonly applied. For equity investments in operating companies, Franco - Nevada estimates attributable emissions by applying its equity ownership percentage to the investee’s reported Scope 1 and Scope 2. However, equity - based attribution approaches are often not well suited to royalty and streaming structures, where Franco - Nevada does not exercise operational control and economic exposure is linked to production from an underlying asset rather than ownership or capital deployed. Following extensive internal analysis and engagement with shareholders, analysts and ESG rating agencies, Franco - Nevada adopted a production - based attribution methodology to estimate Financed Emissions associated with its producing royalty and stream interests. Under this approach, Financed Emissions are estimated by applying Franco - Nevada’s attributable share of production to the reported Scope 1 and Scope 2 emissions of the underlying operations. We believe this methodology provides a transparent, intuitive and repeatable approximation of our proportional exposure to emissions associated with production from the assets in which we hold royalties and streams, while acknowledging the inherent limitations of available data and attribution frameworks. Reported Financed Emissions GHG emissions attributable to Franco - Nevada’s mining and energy interests, classified by the GHG Protocol as Scope 3, Category 15 (Investments), are presented in the adjacent chart and accompanying tables. Financed Emissions are calculated using the methodologies described above and are reported for 2022, 2023 and 2024, reflecting the most recent periods for which sufficient production and emissions data are available from operators. Financed Emissions vary from year-to-year due to changes in total emissions at the underlying operations (measured on a 100% basis), resulting from production levels, operational efficiency, fuel mix and decarbonization initiatives implemented by operators, and Franco - Nevada’s attributable share of production, which may change over time due to variations in metal prices, product mix and the relative contribution of precious - metal by - products to total production. Between 2022 and 2023, our reported Financed Emissions increased primarily due to changes in our attributable share of production at certain producing assets, rather than increases in emissions at the underlying operations. For specific assets, most notably copper operations with precious - metal by - products, our attributable GEOs 1 Includes our Vale debentures and our equity interests in entities that hold royalties on Carol Lake (Labrador Iron Ore Royalty Corporation) and Caserones (Socieded Legal Minera California Una de la Sierra Peña Negra), which we consider as royalty equivalents. 2 Operator emissions and emissions intensities include Scope 1 and 2 emissions. We have relied upon MineSpans for emissions data for producing mining operations. Emissions for non-producing mining and energy operators are deemed to be negligible and have not been included. 3 Includes emissions relating to our working interests over which we do not exercise any control. For certain of our energy royalties and other interests covering large land packages with numerous operators, asset-by-asset emissions estimates are not practicable or available. For consistency, we have calculated all of our Scope 3 emissions from our energy interests using the most accurate publicly available emissions intensities (tCO 2 e/boe) and have applied the volume (boe) received by Franco-Nevada from each operation or region to calculate our attributable emissions. 4 Currently reflects Franco - Nevada’s equity investment in G Mining Ventures Corp. Franco - Nevada also holds other small equity interests in producing mining companies; however, attributable emissions from such holdings have been assessed as negligible and are not included. In addition, Franco - Nevada holds equity and debt investments in mining companies with non - producing projects. Emissions associated with such non - producing projects have likewise not been included, as our proportionate share of emissions based on equity ownership or loan advances is considered de minimis. Mining Interests Energy Interests Equity Interests - 100,000 200,000 300,000 400,000 500,000 600,000 700,000 2024 2023 2022 355,810 142,712 210,119 558,640 146,376 412,264 615,728 156,901 458,827 2,979 Scope 3 Financed Emissions (tCO 2 e) Financed Emissions for mining interests 1 = Operation’s emissions 2 Operation’s GEOs Franco-Nevada GEOs from operation Financed Emissions for equity interests 4 = Franco-Nevada equity ownership percentage Investee Scope 1 emissions Investee Scope 2 emissions Financed Emissions for energy interests 3 = Emissions intensity 2 Franco-Nevada production volume (boe) from operation or region increased year over year, driven largely by commodity price movements, particularly higher gold prices, which affect attribution under the production - based methodology applied to Financed Emissions calculations. Notwithstanding this increase on an attributable basis, Scope 1 and 2 emissions at the underlying operations (on a 100% basis) declined during the period, reflecting emissions - reduction initiatives and operational changes implemented by operators. In contrast, Financed Emissions declined significantly from 2023 to 2024, largely due to the reduced contribution from Cobre Panamá, which accounted for approximately 217,597 tCO 2 e of financed emissions in 2023. The ongoing suspension of operations at Cobre Panamá in 2024 materially reduced its contribution, resulting in a pronounced year - over - year decrease in total Financed Emissions. This illustrates the sensitivity of Financed Emissions to changes in asset - level production status and attribution, in addition underlying asset-level emissions performance. Franco-Nevada Corporation 43

Sustainability Report 2026 Page 44 Page 46

Sustainability Report 2026 Page 44 Page 46